Exciting news for homebuyers as Mortgage Rules change once again

Major updates to mortgage regulations could be a game-changer for homeownership.

These changes are designed to help individuals get closer to owning a home. However, as with any significant policy shift, it's important to consider both sides of the story. Read on to find out what these new rules mean for future homeowners.

important to consider both sides of the story. Read on to find out what these new rules mean for future homeowners.

Here are the Key Changes in Mortgages

Deputy Prime Minister and Finance Minister Chrystia Freeland has announced two fantastic adjustments:

1. Increased Price Cap for Insured Mortgages: The cap is rising from $1 million to $1.5 million. This allows buyers to aim for homes valued up to $1.5 million with a down payment of less than 20%.

2. Extended Amortization Period: The maximum amortization period for insured mortgages is extending from 25 years to 30 years for buyers and those purchasing newly built homes. More time means more flexibility.

These exciting changes will take effect in December 2024, so if you're on the hunt for a new home, keep this info handy as you plan your next steps toward making your dream a reality!

Benefits of the New Mortgage Rules

1. More Homes Within Reach

With the new price cap increase to $1.5 million, Buyers can now explore more options and consider higher price ranges.

2. Lower Monthly Payments

The amortization period extension from 25 to 30 years, homes are more affordable than previously.

For a simplified example:

- Home price: $700,000 - 20% downpayment ($140,000)

- Mortgage amount: $560,000

With a 25-year mortgage: monthly payment = ~$3,034

With a 30-year mortgage: monthly payment = ~$2,756

That’s $278 saved every month!

3. Boost for New Construction

By allowing longer mortgages on newly built homes regardless of whether you're a first-time buyer or not—the government aims to stimulate demand for new housing projects designed to help address Canada’s housing crisis over time.

Drawbacks To Consider

1. More Debt & Interest Costs

While lower monthly payments sound great initially—over time you will pay significantly more interest on your mortgage loan approximately $124k extra over its term. * Note you can change you term when your mortgage renews each time which will save you money in the long run.

2. Slower Equity Building

Longer amortizations mean slower equity growth which may delay future financial goals.

3. Potential For Higher Home Prices

Easier access may drive up prices and lead to more competing offers, especially where supply already lags behind high demand markets.

4. Higher Mortgage Insurance Premiums

Higher loans attract higher premiums adding another layer onto overall debt burden. Keep in mind the simplified example above with 20% down does not have mortgage insurance, anything less than 20% will attract required mortgage insurance premiums.

Read more details about the changes on the Government of Canada website here

The Bigger Picture – What This Means For Our Housing Market Here in Brant?

Who Benefits Most?

First-time buyers, those seeking newly constructed properties; individuals with good incomes but limited savings.

Who Faces Challenges?

High-debt households; competitive pricing areas; near-retirement age groups taking larger long-term debts

Bottom Line:

Get qualified advice. Your neighbour who knows a guy who did so and so does not qualify as good advice.

Ask someone who works in the industry day in and day out.

Do the math comparing the costs between different terms.

Consider your long-term plans and goals.

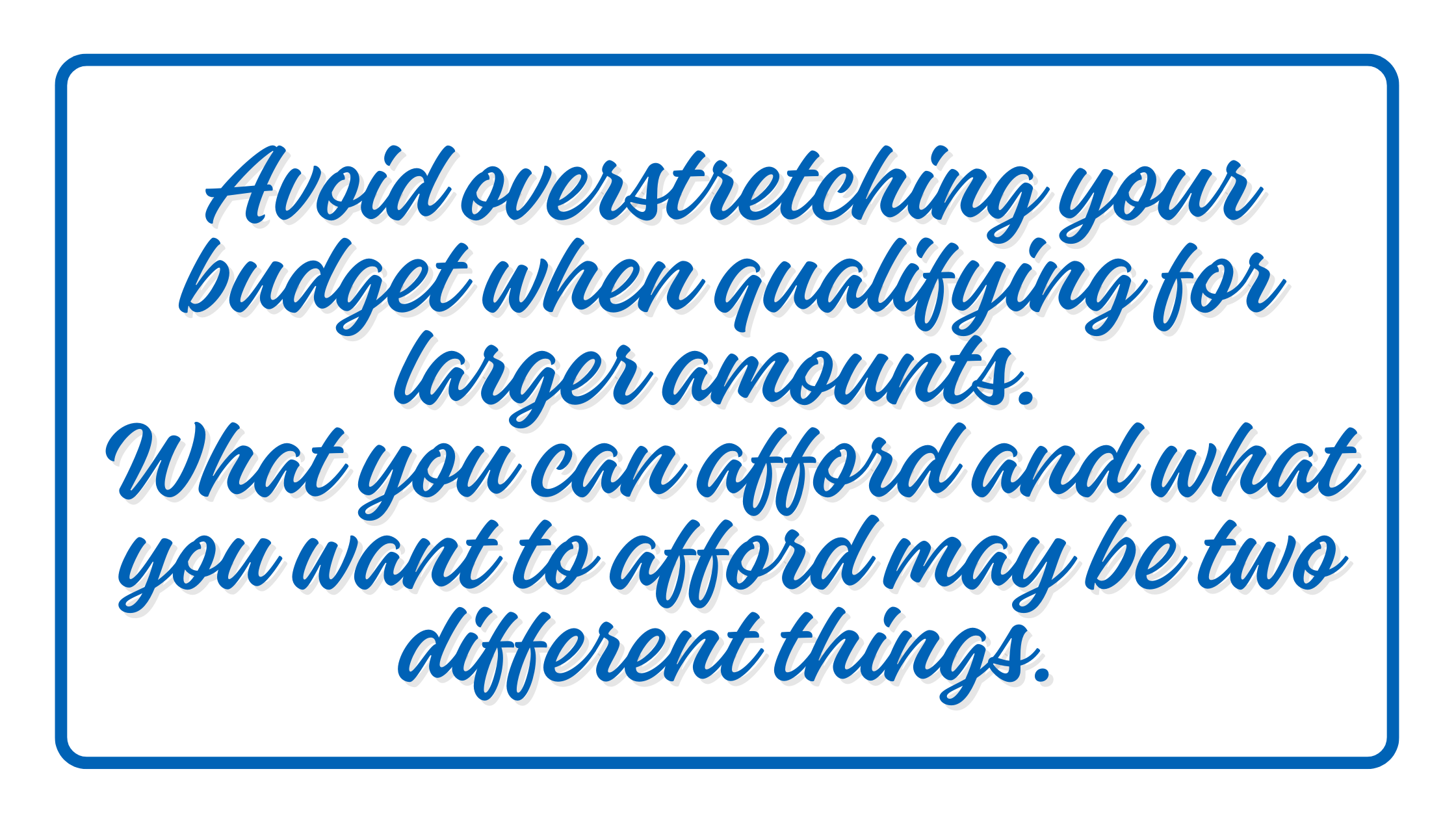

Avoid overstretching your budget when qualifying larger amounts - what you can afford and what you want to afford may be two different things.

Explore various lender offers possibly using brokers securing best deals available.

If you are buying between now and December, talk to a professional to see how the timing will impact your particular situation so you can make informed choices in aligning financial aspirations and lifestyle preferences to ultimately ensure a successful outcome.

Reach out to learn more today and make your home buying dreams a reality on your terms.

Call/text 226-400-6458 or Paula@Tysoski.com

Looking for a new home? You will want to check out our VIP Home Hunter System Here!